The Student Loan Debt Crisis is About to Get Worse: The next generation of graduates will include more borrowers who may never be able to repay.

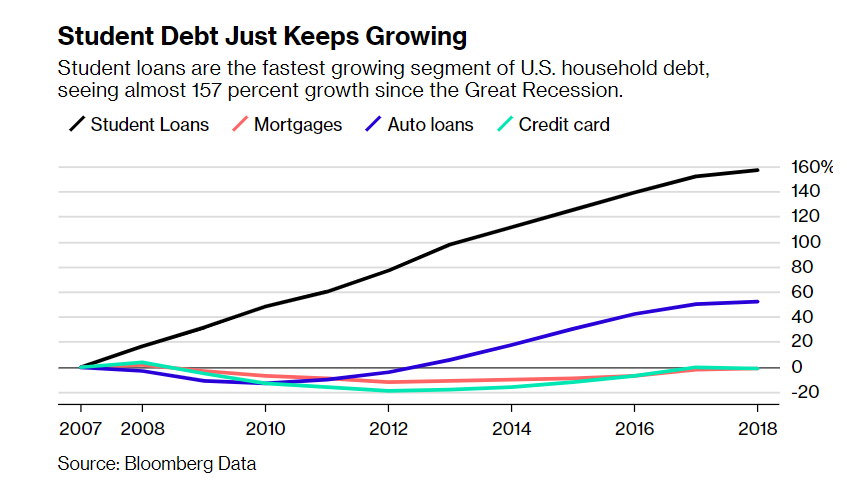

From Bloomberg: Student loans have seen almost 157 percent in cumulative growth over the last 11 years. By comparison, auto loan debt has grown 52 percent while mortgage and credit-card debt actually fell by about 1 percent, according to a Bloomberg Global Data analysis of federal and private loans. All told, there’s a whopping $1.5 trillion in student loans out there (through the second quarter of 2018), marking the second-largest consumer debt segment in the country after mortgages, according to the Federal Reserve. And the number keeps growing.

Student loans are being issued at unprecedented rates as more American students pursue higher education. But the cost of tuition at both private and public institutions is touching all-time highs, while interest rates on student loans are also rising. Students are spending more time working instead of studying. (Some 85 percent of current students now work paid jobs while enrolled.) Experts and analysts worry that the next generation of graduates could default on their loans at even higher rates than in the immediate wake of the financial crisis.